Erasmus Management Lecture

Donald Bergh: Value Creation in Restructuring: A Strategic Perspective

26 June 2015

How can corporate restructuring create value for firms and their stakeholders? Applying a strategic perspective, Donald Bergh, Louis D. Beaumont Professor of Business Administration and Professor of Management at the Daniels College of Business, University of Denver presented common motivations for restructuring actions, the implementation process through which they occur, their associations with firm performance, and relationships with integrating corporate and business strategies. A panel of invited academics offered their insights into the pragmatics of managing restructuring and sparked lecture participants to challenge four propositions put forth in the lecture.

Text Joey Johannsen | Photos Chris Gorzeman

The Erasmus Management Lecture presents distinguished scholars to an audience of doctoral students, faculty and industry representatives. The guest scholar provides a public lecture on a stimulating topic where academic knowledge and practical relevance meet. Typically, the Erasmus Management Lecture is combined with a short course for doctoral students and junior faculty in the ERIM Summer School. Lecturers are invited in recognition of their contributions and impact to their respective research fields.

Restructuring increasingly popular with Dutch corporations

Professor Bergh outlined his agenda after providing a local summary of some Dutch firms that have been in the news due to their involvement in the process of restructuring since 2010.

Unilever, Phillips, Royal Dutch Shell, Koninklijke Ahold, and AEGON, among others, have used large-scale reductions in product lines, divestitures, acquisitions, refocusing, spinoffs and equity carve outs to shape their corporate portfolios and to strengthen their performance outcomes. Bergh confirmed that such actions are gaining in their popularity and presence throughout the international business community.

Bergh focused on the divestiture side of portfolio restructuring, with a clear intent to inspire research in this area. He identified four key motivations that lead a company to consider restructuring: environmental (uncertainty, social pressures, global competition and market trends), owners (market for corporate control, pressuring changes, performance resolution, heightened monitoring, board initiated restructuring), strategic (reverse acquisition mistakes, over-diversified, refocus core business, correct market de-valuation, post-acquisition resource deployment) and organisational (overly complex, loss of control, change in leadership).

Professor Bergh further described these motivations through the lens of a manager or a firm owner with a strategic perspective. They served as the premise for four propositions the panel debated at the close of the lecture.

The invited panellists took to the floor after Bergh introduced historic theories of value creation: Transaction cost economics (when hierarchical efficiency is regained), Agency theory (the most dominant theory showing value is created when diversification discount is resolved), and Resource-based view (where, according to Bergh, the most potential lies). He then briefly explained how to use these theories as foundational territory to interpret current trends and contemporary issues.

Panellists

Pursey Heugens, Professor of Organisation Theory, Development, and Change, Department of Strategic Management and Entrepreneurship, Rotterdam School of Management, Erasmus University, moderated the panel discussion, inviting Professor Bergh to respond to comments offered by Xavier Martin, Professor of Strategy, International Business and Innovation, Deputy Head of the Department of Management, Tilburg University, and Hans van Oosterhout, Professor of Corporate Governance and Responsibility, and Chair of the Department of Strategic Management and Entrepreneurship, Rotterdam School of Management, Erasmus University.

Key Issues

Owners are frequently portrayed as pressuring managers to use restructuring actions to improve firm performance. Does this ownership pressure create value for the firm, the owners, both, or neither?

Professor Bergh’s position is that owners tend to gain financially from restructuring actions but serving their interests may present managers with serious challenges for sustaining growth. He responded to Professor Heugens example of PepsiCo and GE Capital ownership by insisting owners need to let managers work and stop pressuring managers with restructuring just to solve owner problems. “Owners are best at managing portfolios of investment”, he declared, such as Jack Welch, who is considered manager of the century. A focus on the bottom line, on the other hand, provides little to help a firm sustain long-term strategic improvements, says Bergh. Instead he challenged the audience to look at context, the full industry, and to have a long-term investment view.

Restructuring is often used to de-diversify firms, to narrow their overall holdings and increase their focus and specialisation. When is this change in strategy likely to create value and when is it not?

Professor Martin emphasized that restructuring often implies a firm has taken on more than it should and is better off adjusting differently. He presented three anchor examples of three Dutch companies. The first, DSM, was successful in restructuring from a dying petro-chemical company to a company focused on life sciences, which made them enter the top 3 position of its industry. He added it was not only restructuring that helped here, but also a move from macro to micro science; DSM abandoned what they were previously doing. A second example was Philips. With a declining stock market Philips got out of the lighting business and started anew with innovative technologies. The third and final example that Professor Martin presented was Royal Dutch Shell. “They are a 170 billion dollar stock market power with nowhere to go," he added. "Their carbon-based company is stuck in profit. The stock market can help, but we need to ponder this.”

In Professor Bergh's words, “the call to become lean and mean seems convincing, a silver bullet for business success. However, we need to understand the way that diversification is related to performance. The literature is expansive in this area." He referenced, for example, Alfred D. Chandler’s 1962 book Strategy and Structure, which is still hugely popular. “The literature of the 1980s shows the benefits of combining strategy and structure.” Restructuring to an intermediate level of diversification would likely be more beneficial than using it refocus around a very narrow or specialized set of businesses.

Restructuring is often conducted through sell-offs and spin-offs. Under what conditions does each mode/alternative create value?

Professor Bergh defined sell-offs as an "exchange of asset ownership from one firm to another" and spin-offs as divestitures whereby "Separate subsidiary/divisions of a company become independent." Professor Hans van Oosterhout raised the issue of contextualisation to the conversation. He reminded us that the Netherlands has low levels of layoffs and relocations. "Context affects restructuring", he stated. In Europe there are more family owners. In response Professor Bergh challenged that, "owners have a profit drive. Owners tend to favour less diversified firms. In general, owners prefer spin-offs and managers prefer sell-offs; for owners, spin-offs provide them with choice on whether to hold or sell their shares in either the divesting or spun-off business while sell-offs can be auctioned off to maximize sales price and give managers more proceeds to reinvest or pay down debt."

He continued, saying, "Overall, spin-offs are typically used to rid a firm of a core business, such as a supplier or distributor, while sell-offs are used to exit non-core and unrelated business altogether. Spin-offs permit the divesting and divested business to retain a post-divestiture relationship while sell-offs tend to end the association.” Maximizing the value of either divestiture mode depends on the motivation and strategic relationship of the assets involved.

Restructuring through spin-offs create a new, independent business that operates separately from the restructuring firm. Do these firms benefit more from a complete "cut" from the restructuring firm or when it retains an active involvement, identity, and interest?

Professor Bergh pointed out that part of PepsiCo's value comes from the ownership of Frito Lay. Frito Lay has a market share of 55% in the snack food industry. While it contributes to the global social problem of obesity, it is profitable. Stakeholders challenge the association to the main product, Pepsi, and would like to see Frito Lay cut from the fold, to create an independent business model. Profit locks it in.

With spin-offs, "the apple does not fall far from the tree." If parents did well with a business, their company's spin-off generally does well too. It is a signal that leads to proactive restructuring. So, post-divestiture imprints from the parent, including sharing the parent firm’s name, having some of its executives migrate over, continuing an ownership stake, take greater meaning when considered within an inheritance perspective. If the spin-off is coming from a high performing parent, then it tends to benefit from the parent’s association. And evidence exists for the opposite as well.

The Bigger Issue

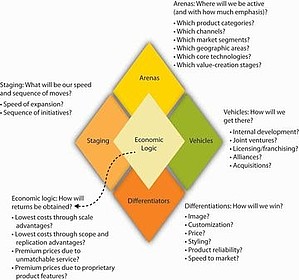

The bigger issue Bergh stressed in his lecture is answering the question, “What do we mean by strategy?” He presented the Strategy Diamond Model designed by Hambrick and Fredrickson[1] to help us begin to refocus our restructuring discussion. Bergh suggested to bring the corporate view down to the business strategy level. In addition, he referred to the six key evaluation criteria for testing the quality of a firm's strategy, as suggested by Hambrick and Fredrickson by clarifying that “viewed from this perspective, restructuring becomes a way of improving the firm’s strategy and hopefully allowing it to compete more effectively.”

Lack of a long-term view in divestiture research

Professor Bergh’s overall conclusion is that, “restructuring creates value when it repositions a firm to more profitable segments in its industry; improving its competitive advantage”. Repositioning is more likely to create value and improve a firm’s competitive advantage when it allows for sustainability of differentiators, refocuses to moderate levels of diversification strategy, blends financial and strategic controls and aligns mode with ownership, experience and strategy. In closing, Bergh proclaimed that “divestitures are not a sexy research theme”, but expressed hope there will be a spark for more in-depth research on the topic. As a follow-up, he insisted upon “the importance of developing an integrative perspective; of linking theories together and also different levels of thinking, both corporate and business.” We should be interested in learning how companies benefit over time. He encouraged researchers to apply a long-term investment and resource view.